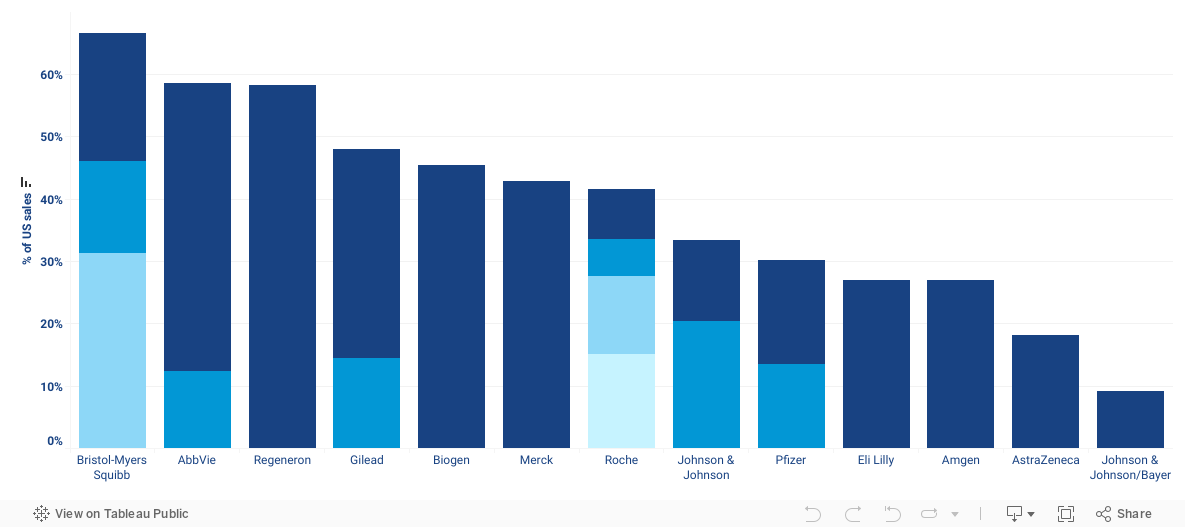

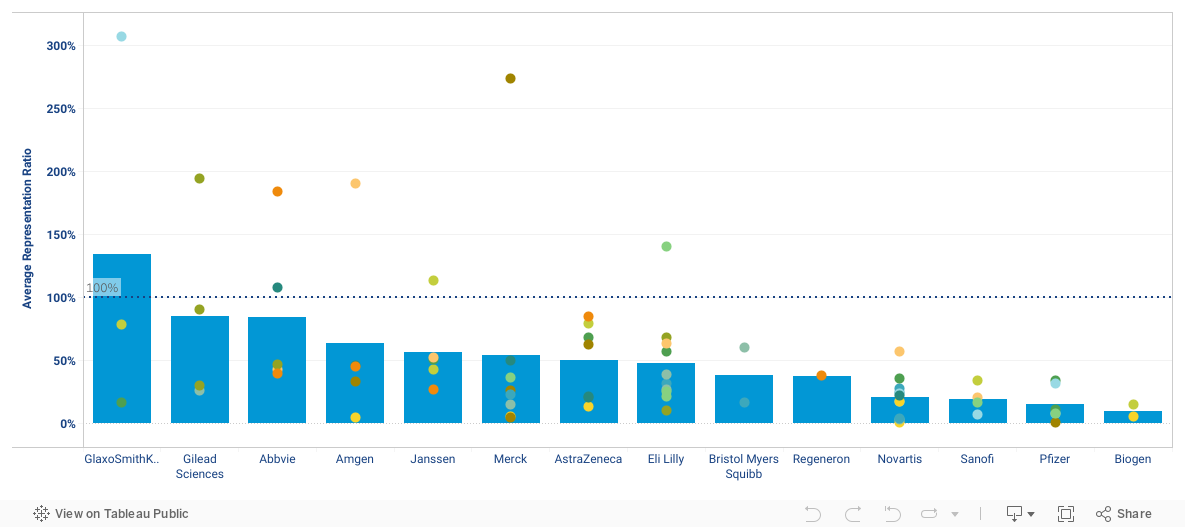

Many of the largest pharmaceutical companies derive an outsize share of their revenues from a single product. In several cases, this is a direct result of successful efforts to delay generic competition, as discussed in Abuses of Government Programs and Regulations. In other situations, companies are directing R&D dollars toward expanding indications or creating new formulations of existing products, which is inherently lower risk than developing new drugs and has the benefit of layering additional periods of exclusivity on prized franchises.

In recent years, this practice has been particularly common in oncology and immunology. Revlimid, for example, is a minor improvement over its predecessor Thalomid, but has managed to have 15 years of market exclusivity.1 For biologics, several of these franchises have just starting facing biosimilar competition. Roche’s Avastin and Rituxan make up over 20% of their manufacturer’s sales, and Tecfidera makes up over 40% of Biogen’s sales in 2020.